Introduction

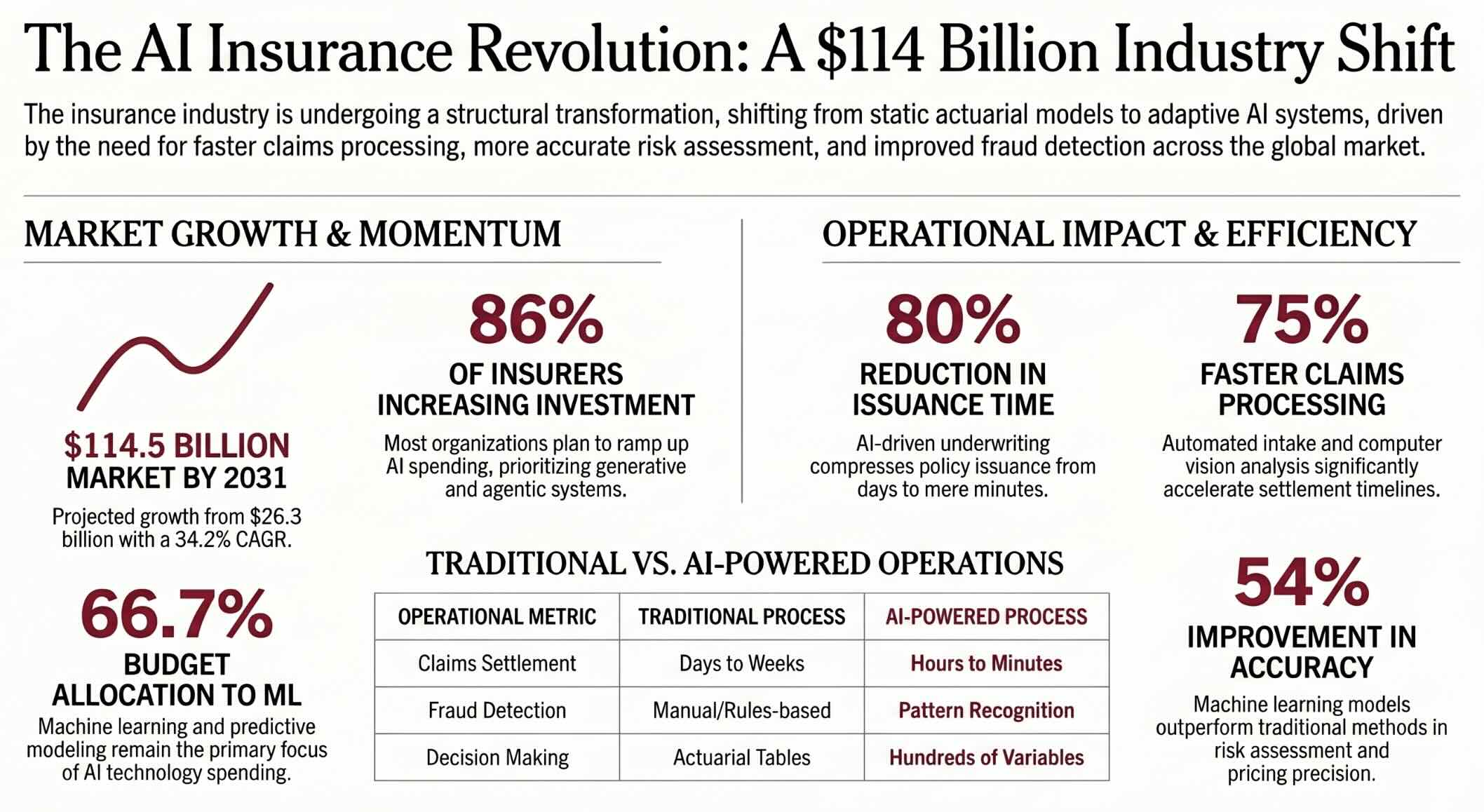

The insurance industry sits on one of the largest reservoirs of structured data in the global economy, and artificial intelligence is unlocking its value at an unprecedented pace. According to Mordor Intelligence’s 2026 market analysis, the AI in insurance market is projected to grow from $26.3 billion in 2026 to $114.52 billion by 2031, registering a compound annual growth rate of 34.2%. That trajectory reflects a fundamental shift in how insurers assess risk, process claims, detect fraud, serve customers, and design products. From machine learning models that evaluate thousands of data points in milliseconds to natural language processing tools that read and interpret policy documents, AI is embedded across every stage of the insurance value chain. Insurers that fail to adopt these technologies risk falling behind competitors who can price more accurately, settle claims faster, and deliver personalized experiences that today’s consumers expect. This article explores what artificial intelligence means in the insurance context, the specific technologies driving adoption, and the practical applications reshaping one of the world’s oldest industries.

Essential Answers on AI in Insurance

What is artificial intelligence in insurance?

Artificial intelligence in insurance refers to the use of machine learning, natural language processing, computer vision, and predictive analytics to automate and improve underwriting, claims processing, fraud detection, pricing, and customer service across the insurance value chain.

How does AI improve insurance claims processing?

AI accelerates claims processing by automatically extracting information from submitted documents, photos, and videos, analyzing damage through computer vision, and routing claims for faster settlement, reducing resolution times from weeks to hours.

What are the biggest risks of using AI in insurance?

The primary risks include algorithmic bias that can lead to unfair pricing or coverage denials, data privacy vulnerabilities from processing sensitive personal information, regulatory uncertainty, and over-reliance on automated decisions without adequate human oversight.

Key Takeaways

- Responsible AI adoption requires addressing algorithmic bias, data privacy, regulatory compliance, and maintaining human oversight in consequential decisions.

- AI in insurance is projected to grow from $26.3 billion in 2026 to over $114 billion by 2031, driven by demand for automated underwriting, claims processing, and fraud detection.

- Machine learning, natural language processing, computer vision, and predictive analytics are the four foundational AI technologies transforming insurance operations.

- Insurers using advanced AI report up to 75% faster processing speeds, 54% improvement in underwriting accuracy, and 30% reductions in fraudulent claims payouts.

Table of contents

- Introduction

- Essential Answers on AI in Insurance

- Key Takeaways

- Defining Artificial Intelligence in the Insurance Context

- Core AI Technologies Powering Modern Insurance

- How Machine Learning Transforms Risk Assessment

- The Role of Natural Language Processing in Policy Management

- Computer Vision and Visual Claims Analysis

- AI-Powered Underwriting and Pricing Models

- Streamlining Claims Processing with Intelligent Automation

- Fraud Detection Through Pattern Recognition and Analytics

- Chatbots, Virtual Assistants, and Customer Experience

- Telematics, IoT, and Usage-Based Insurance

- Predictive Analytics for Loss Prevention

- The Data Challenge in Insurance AI Adoption

- Algorithmic Bias and Fairness in Insurance Decisions

- Regulatory Landscape for AI in Insurance

- Privacy, Security, and Ethical Considerations

- Embedded Insurance and Parametric Models

- Building an AI-Ready Insurance Organization

- The Future of Artificial Intelligence in Insurance

- Key Insights

- How AI Transforms Insurance Operations: A Comparative View

- Real World Examples Of AI In Insurance

- Case Studies

- Frequently Asked Questions About Artificial Intelligence in Insurance

Defining Artificial Intelligence in the Insurance Context

Artificial intelligence in insurance is the application of computational systems that learn from data, recognize patterns, and make predictions or decisions to automate and enhance core insurance functions including underwriting, claims management, fraud detection, pricing, and customer engagement.

AI in Insurance Impact Explorer

See how AI transforms insurance operations across functions. Select a use case, adjust adoption level and company size, and explore projected impact metrics.

The insurance industry has always been a data-driven business, relying on actuarial tables, historical loss data, and statistical models to price risk and manage reserves. What distinguishes the current AI transformation from earlier waves of digitization is the ability of modern systems to process unstructured data, learn from outcomes, and improve their own performance without explicit reprogramming. Traditional rule-based systems could flag a claim that exceeded a dollar threshold, but they could not read the narrative description of an accident, analyze photographs of vehicle damage, cross-reference the claimant’s history, and assess the probability of fraud in a single automated workflow. AI makes that kind of integrated analysis possible by combining multiple technologies into systems that approximate human judgment at machine speed and scale. The shift from static rules to adaptive intelligence represents the most significant operational transformation the insurance industry has experienced since the introduction of computerized databases in the 1970s. Insurers that understand the distinction between automation and true AI are better positioned to deploy these technologies where they create the greatest value.

The practical scope of AI in insurance extends across the entire policy lifecycle, from initial marketing and lead scoring through underwriting, policy issuance, premium collection, claims handling, and renewal or cancellation. Each stage generates data that feeds back into the system, creating a continuous learning loop that improves accuracy and efficiency over time. A machine learning model that processes millions of claims learns to identify patterns that predict future losses with increasing precision, enabling insurers to price policies more competitively while maintaining profitability. Natural language processing tools read emails, chat transcripts, and policy documents to extract relevant information and route it to the appropriate department without human intervention. Computer vision algorithms assess property damage from drone footage or smartphone photographs, generating repair estimates that once required an in-person adjuster visit. The cumulative effect of these applications is not incremental improvement but a structural reshaping of how insurance companies operate, compete, and deliver value to policyholders.

Core AI Technologies Powering Modern Insurance

The AI revolution in insurance rests on four foundational technologies that work independently and in combination to address different operational challenges across the value chain. Machine learning, the most widely deployed technology, uses algorithms that learn from historical data to make predictions and decisions without being explicitly programmed for each scenario. Natural language processing enables computers to read, interpret, and generate human language, powering applications from chatbot interactions to automated policy document analysis. Computer vision allows systems to interpret and analyze visual information from images, video, and satellite feeds, enabling remote damage assessment and property inspection at scale. Each technology addresses a distinct category of insurance problems, and the most sophisticated deployments integrate all four into unified platforms that can handle complex, multi-step workflows.

Machine learning forms the backbone of modern insurance analytics, and understanding its theoretical foundations helps clarify why it has become so central to the industry’s transformation. Supervised learning models trained on labeled historical data predict outcomes like claim severity, policy lapse probability, and fraud likelihood with accuracy rates that exceed traditional statistical methods. Unsupervised learning algorithms identify hidden patterns in customer behavior, claims data, and market dynamics that human analysts might never detect. Reinforcement learning systems optimize pricing strategies by testing different premium structures and learning from market responses over time. The insurance industry’s enormous historical datasets make it an ideal environment for machine learning because the algorithms improve with more data, and insurers have decades of claims, underwriting, and customer interaction records to feed into their models. Research indicates that insurers allocate approximately 66.7% of their AI budgets to traditional machine learning and predictive modeling, reflecting its foundational importance.

Natural language processing and computer vision represent the next frontier of insurance AI adoption, handling the unstructured data that traditional analytics could not touch. Approximately 80% of insurance data exists in unstructured formats: handwritten notes, medical records, police reports, photographs, videos, and free-text communications between agents and policyholders. NLP tools parse this information, extract key entities like dates, amounts, diagnoses, and policy numbers, and convert it into structured data that downstream systems can process. Computer vision analyzes images of damaged vehicles, flooded properties, hail-impacted roofs, and medical scans to assess severity, estimate repair costs, and detect visual indicators of fraud such as pre-existing damage. Together, these technologies allow insurers to automate processes that previously required human experts to read, interpret, and make judgment calls on thousands of individual documents and images each day.

Predictive analytics ties these technologies together into forward-looking systems that anticipate outcomes rather than merely reacting to events after they occur. By combining historical data with real-time inputs from IoT sensors, weather feeds, economic indicators, and behavioral signals, predictive models forecast which policyholders are most likely to file claims, which properties face elevated natural disaster risk, and which customer segments are at risk of lapsing. The ability to act on these predictions, adjusting pricing, reallocating reserves, targeting retention efforts, and deploying loss prevention resources before losses materialize, transforms insurance from a reactive reimbursement business into a proactive risk management partner. Insurers that have embraced predictive analysis as a strategic capability report measurable improvements in loss ratios, customer retention, and operational efficiency, creating competitive advantages that compound over time.

How Machine Learning Transforms Risk Assessment

Risk assessment has always been the core function of the insurance industry, and machine learning is fundamentally changing how insurers evaluate the likelihood and potential severity of future losses. Traditional underwriting relied on broad actuarial categories, grouping applicants by age, location, credit score, and claims history into risk pools that applied average pricing to individuals whose actual risk profiles varied enormously within each group. Machine learning models analyze hundreds or thousands of variables simultaneously, identifying nonlinear relationships and interaction effects that human underwriters and linear statistical models cannot detect. A model evaluating a commercial property risk might simultaneously consider building materials, fire department response times, nearby chemical facilities, historical weather patterns, tenant financial stability, and satellite imagery of the surrounding area to produce a risk score that is both more granular and more accurate than traditional methods.

The speed advantage of machine learning in underwriting is as significant as the accuracy improvement, compressing processes that once required days into minutes or seconds. Research from Deloitte indicates that AI-driven underwriting can reduce policy issuance times by up to 80%, allowing insurers to serve more customers while reducing the operational cost per policy. Applicants submitting straightforward personal auto or homeowner’s insurance applications can receive quotes almost instantaneously, a customer experience that was impossible when every application required manual review. Complex commercial risks still benefit from human expertise, but machine learning handles the data gathering, preliminary analysis, and risk scoring that consumed most of an underwriter’s time, freeing them to focus on the judgment-intensive aspects of unusual or high-value accounts. AI does not replace the experienced underwriter; it amplifies their capacity by handling the analytical workload that previously limited the number of risks they could evaluate in a given day.

The evolution from static risk models to dynamic, continuously learning systems represents a paradigm shift in how insurers understand and price uncertainty. Traditional actuarial models were recalibrated annually or quarterly, meaning that emerging risk trends could take months to reflect in pricing. Machine learning models can be retrained continuously as new data arrives, adapting to shifting patterns in claims frequency, severity, and customer behavior in near real time. This responsiveness is particularly valuable in volatile lines of business like cyber insurance, where the threat landscape changes weekly, and in catastrophe-exposed regions where climate patterns are shifting faster than historical data can capture. Deep learning architectures enable even more sophisticated modeling of complex risk interdependencies, though their computational demands and interpretability challenges require careful evaluation before deployment in regulated insurance environments.

The Role of Natural Language Processing in Policy Management

Natural language processing is quietly transforming the administrative backbone of insurance operations, automating the reading, writing, and interpretation of the vast document ecosystem that defines the industry. Insurance generates enormous volumes of text: policy wordings, endorsements, exclusion schedules, claims narratives, adjuster reports, correspondence, regulatory filings, and coverage opinions that collectively run to millions of pages across a single large carrier. NLP tools trained on insurance-specific language can extract key clauses, identify coverage triggers, compare policy versions, and flag inconsistencies with a speed and consistency that manual review cannot match. The technology handles tasks that paralegals, claims adjusters, and underwriting assistants traditionally performed, not by replacing their judgment but by eliminating the hours of reading and data extraction that preceded each decision point.

Policy comparison and coverage analysis represent high-value NLP applications that directly affect underwriting quality and claims accuracy. When a broker submits a submission package containing incumbent policy documents, loss runs, and supplemental applications, an NLP system can extract every coverage detail, limit, deductible, endorsement, and exclusion from the existing program and present it in a structured comparison format within minutes. This capability is particularly valuable in complex commercial and specialty lines where policies run to hundreds of pages and subtle differences in wording can determine millions of dollars in claim outcomes. Carriers that have deployed NLP solutions understand both the power and the challenges of applying language technology to an industry where a single word in a policy exclusion can change the outcome of a multi-million dollar claim. The precision required in insurance language processing sets a higher bar than general-purpose NLP applications because the cost of misinterpreting a policy provision is measured in claim payments, regulatory penalties, and litigation exposure.

Computer Vision and Visual Claims Analysis

Computer vision is revolutionizing the way insurers assess physical damage, inspect properties, and verify the conditions reported in claims, transforming processes that historically required human adjusters to travel to the scene of every loss. When a policyholder submits photographs of a damaged vehicle after an accident, computer vision algorithms can identify the affected panels, estimate the severity of dents and scratches, cross-reference the damage patterns against a database of known repair procedures, and generate a preliminary repair estimate in seconds. The same technology analyzes aerial drone footage of roofs damaged by hail storms, identifying impact marks and estimating the percentage of the roof surface that requires replacement without sending an adjuster to climb a ladder. These capabilities reduce cycle times dramatically while improving consistency, because an algorithm applies the same assessment criteria to every image rather than introducing the variability inherent in different human adjusters’ experience and judgment.

Property inspection and pre-loss documentation represent growing applications of computer vision that extend beyond claims into underwriting and risk engineering. Insurers use satellite imagery and machine learning to assess property conditions at scale, identifying features like roof age, vegetation proximity, swimming pools, and structural modifications that affect risk without requiring a physical inspection. Flood risk models incorporate topographic data, drainage patterns, and historical flood imagery to refine exposure assessments at the individual property level. Commercial insurers deploy computer vision in manufacturing facilities and construction sites to identify safety hazards, monitor compliance with risk engineering recommendations, and verify that loss prevention improvements have been implemented. The combination of computer vision with drone technology and satellite feeds gives insurers a persistent, scalable surveillance capability that would be economically impossible to achieve through human inspection alone. The technology works best as a triage tool that handles routine assessments automatically while flagging complex or ambiguous cases for human expert review.

Fraud detection benefits significantly from computer vision’s ability to identify visual anomalies and inconsistencies that human reviewers might miss, particularly when processing high volumes of claims simultaneously. An algorithm trained on millions of vehicle damage images can detect signs of pre-existing damage, inconsistent damage patterns relative to the reported accident description, and visual cues associated with staged collisions. Property claims analyzers can compare pre-loss and post-loss imagery to verify that reported damage is consistent with the claimed event and did not exist before the policy was issued. These automated checks run in the background of the claims workflow, scoring each submission for fraud indicators and escalating suspicious cases for investigation without delaying the processing of legitimate claims. The approach reduces false positive rates compared to rules-based fraud flags while catching sophisticated schemes that exploit the sheer volume of claims flowing through traditional manual review processes.

AI-Powered Underwriting and Pricing Models

Artificial intelligence is enabling a new generation of underwriting and pricing models that move beyond broad actuarial categories toward individualized risk assessment and dynamic premium calculation. Traditional pricing relied on a limited set of rating variables, applying the same premium to everyone within a given classification who shared similar demographic and historical characteristics. AI models incorporate hundreds of additional data points, from credit-based insurance scores and driving telematics to social media activity and IoT sensor readings, producing risk profiles that more accurately reflect each individual’s likelihood of filing a claim. This granularity benefits both insurers, who can price more profitably by avoiding adverse selection, and low-risk policyholders, who pay premiums that reflect their actual behavior rather than subsidizing the losses of higher-risk members of their rating group.

Dynamic pricing represents the frontier of AI-powered insurance economics, where premiums adjust continuously based on real-time behavioral data rather than remaining fixed for the duration of a policy term. Usage-based auto insurance programs already adjust rates based on telematics data that tracks driving behavior including speed, acceleration, braking, cornering, and time of day. Health insurers experiment with wearable device data that rewards policyholders for maintaining activity levels, sleep quality, and preventive care compliance. Commercial property insurers integrate IoT sensor data from building management systems, fire suppression equipment, and security networks to offer premium credits for facilities that demonstrate superior risk management practices. The transition from static annual pricing to continuous, behavior-based premium adjustment represents a fundamental reconceptualization of the insurance contract, shifting from a backward-looking bet on historical averages to a forward-looking partnership that rewards proactive risk reduction. The role of AI in boosting automation across pricing workflows extends beyond simple calculation to encompass the entire decision architecture that determines what a policyholder pays.

Streamlining Claims Processing with Intelligent Automation

Claims processing has traditionally been the most labor-intensive and customer-sensitive function in insurance operations, and AI is compressing timelines that once stretched for weeks into periods measured in hours or days. The claims journey begins with first notice of loss, where policyholders report incidents through phone calls, mobile apps, or web portals. AI-powered intake systems use natural language processing to extract key details from verbal descriptions or written submissions, categorize the claim type, identify the applicable policy and coverage, and initiate the appropriate workflow without requiring a human to read and route each submission manually. This automation eliminates the bottleneck that historically caused backlogs during catastrophe events, when thousands of claims arrived simultaneously and overwhelmed human intake capacity.

Damage assessment and reserve estimation represent the analytical core of claims processing, and machine learning models are improving both the speed and accuracy of these critical steps. When a vehicle damage claim arrives with photographs, computer vision generates a preliminary estimate while machine learning models predict the total cost based on similar historical claims, vehicle type, parts availability, and regional labor rates. Property claims triggered by natural disasters benefit from satellite imagery analysis that assesses damage across entire affected areas, prioritizing the most severely impacted properties for expedited processing. Medical claims in health and workers’ compensation lines use predictive models to estimate treatment duration, anticipated costs, and return-to-work timelines based on diagnosis codes, provider patterns, and patient demographics. Insurers deploying these systems report processing speed improvements of up to 75% while maintaining or improving accuracy, creating a customer experience that builds loyalty and reduces the friction that historically drove complaints and regulatory action.

The integration of AI into claims creates opportunities for straight-through processing, where routine, low-complexity claims are evaluated, approved, and paid without any human intervention. A minor vehicle damage claim with clear photographic documentation, consistent policyholder narrative, no fraud indicators, and a repair estimate within established thresholds can move from first notice of loss to payment in hours. Insurance technology companies like Lemonade have built their business models around this capability, promoting claim settlement times measured in seconds for qualifying submissions. The challenge for traditional carriers is integrating AI-driven automation into legacy systems and workflows that were designed around human decision-making at every stage, a transformation that hyperautomation frameworks are designed to address. Straight-through processing works best for standardized, high-frequency, low-severity claims, while complex, high-value, or disputed claims continue to require human expertise in investigation, negotiation, and judgment.

Fraud Detection Through Pattern Recognition and Analytics

Insurance fraud costs the industry tens of billions of dollars annually, and AI-powered detection systems are fundamentally changing how carriers identify, investigate, and prevent fraudulent activity across all lines of business. The FBI estimates that non-health insurance fraud costs more than $40 billion per year in the United States alone, a figure that translates directly into higher premiums for honest policyholders. Traditional fraud detection relied on rules-based systems that flagged claims matching predefined criteria, an approach that generated high volumes of false positives while missing sophisticated schemes that did not fit established patterns. Machine learning models trained on historical fraud data learn to identify subtle combinations of indicators that collectively suggest fraudulent intent, catching schemes that rules-based systems overlook while reducing the investigation burden on special investigation units.

Modern fraud detection deploys multiple AI techniques in parallel to create layered defenses that address different fraud vectors simultaneously. Machine learning models analyze applicant and claimant data against known fraud patterns, checking whether an address has appeared in multiple suspicious claims, whether the timing and circumstances of a loss follow patterns associated with staged events, or whether the claimant’s financial situation suggests motive. Behavioral analytics scrutinize how applications are completed and how claimants answer questions, flagging hesitation patterns, inconsistent narratives, and other behavioral cues that correlate with deception. NLP algorithms read written statements, medical records, and repair estimates to identify inconsistencies in language, temporal sequencing, and factual details that contradict the physical evidence. The multi-layered approach means that a fraudster who successfully evades one detection method is likely to trigger another, creating a defense-in-depth architecture that makes successful fraud increasingly difficult and economically irrational.

Social network analysis adds another dimension to AI fraud detection by mapping relationships between claimants, witnesses, medical providers, repair shops, and legal representatives to identify organized fraud rings. A single suspicious claim might not trigger investigation, but when AI reveals that the same attorney, body shop, and medical clinic appear in dozens of claims with similar characteristics filed by individuals connected through social or professional networks, the pattern becomes unmistakable. Link analysis tools visualize these connections, enabling investigators to understand the scope and structure of fraud networks that would be invisible through individual claim review. Insurers that have deployed comprehensive AI-driven cybersecurity and fraud prevention frameworks report reducing fraudulent claims payouts by approximately 30%, translating directly into lower loss ratios and more competitive premiums for legitimate policyholders.

Chatbots, Virtual Assistants, and Customer Experience

Artificial intelligence is reshaping the customer experience in insurance through conversational AI systems that handle routine interactions with speed and availability that human agents cannot match economically. Insurance chatbots and virtual assistants answer policy questions, provide quotes, process endorsements, accept premium payments, file first notices of loss, and guide policyholders through the claims process around the clock in multiple languages. These systems use natural language understanding to interpret customer inquiries expressed in everyday language rather than insurance terminology, making the interaction accessible to policyholders who may not understand the technical distinctions between coverage types or policy provisions. The cost advantage is substantial: a virtual assistant can handle thousands of simultaneous conversations at a fraction of the cost of staffing a call center with enough human agents to eliminate hold times during peak periods.

The evolution of insurance chatbot technology extends beyond simple question-answering into proactive engagement and personalized service delivery. Modern AI assistants analyze a customer’s policy portfolio, claims history, and life events to offer timely recommendations, such as suggesting additional coverage when a policyholder adds a new driver or purchases a home. They detect sentiment shifts during conversations, escalating to human agents when frustration, confusion, or emotional distress signals indicate that automated responses are insufficient. Proactive renewal reminders, personalized coverage reviews, and automated policy comparison tools transform the customer relationship from transactional to advisory, increasing retention and cross-selling opportunities. The most effective insurance chatbot deployments use AI not to eliminate human interaction but to ensure that human expertise is directed toward the conversations where it creates the most value, such as complex claims negotiations, sensitive coverage consultations, and high-value account management. Customer satisfaction scores in AI-enabled insurance interactions have improved by 15 to 20% where insurers have implemented these systems thoughtfully.

Telematics, IoT, and Usage-Based Insurance

The convergence of artificial intelligence with Internet of Things technology is enabling insurance products that price risk based on real-time behavior rather than static demographic categories, representing one of the most fundamental shifts in insurance product design in decades. Telematics devices installed in vehicles or accessed through smartphone apps collect data on driving speed, acceleration, braking intensity, cornering force, time of day, route selection, and total miles driven, feeding this information into machine learning models that calculate a personalized risk score for each policyholder. Safe drivers who avoid aggressive maneuvers, limit late-night driving, and maintain consistent speeds benefit from significantly lower premiums than they would receive under traditional rating plans that average risk across broad demographic groups. The model creates a direct financial incentive for safer behavior, aligning the insurer’s interest in reducing losses with the policyholder’s interest in paying lower premiums.

Smart home devices extend the IoT insurance model beyond vehicles into property coverage, where sensors detect water leaks, smoke, carbon monoxide, temperature extremes, and security breaches in real time, enabling insurers and policyholders to prevent losses before they occur. A water leak sensor that detects moisture accumulation behind a washing machine and alerts the homeowner through a smartphone notification can prevent tens of thousands of dollars in water damage that the insurer would otherwise pay as a claim. Insurers offer premium discounts or free sensor packages to incentivize adoption, recognizing that the reduction in claims cost far exceeds the cost of the devices. The data generated by these sensors feeds back into predictive maintenance and loss prevention models that identify properties at elevated risk of specific loss types, enabling targeted outreach before damage occurs.

Wearable health devices represent the next frontier of IoT-enabled insurance, creating opportunities for health and life insurers to reward policyholders who maintain healthy behaviors with lower premiums and enhanced benefits. Fitness trackers and smartwatches monitor activity levels, heart rate variability, sleep quality, and other biometric indicators that correlate with long-term health outcomes and mortality risk. Life insurers offer accelerated underwriting programs that use wearable data in combination with electronic health records and prescription databases to issue policies without requiring traditional medical examinations, reducing issuance times from weeks to days. The combination of IoT data collection, AI-powered analysis, and dynamic pricing creates a new insurance paradigm where the product adapts continuously to the policyholder’s behavior, transforming insurance from a static contract into an ongoing risk management partnership. The challenge lies in balancing the benefits of personalized pricing with concerns about surveillance, data privacy, and the potential for discriminatory outcomes when granular behavioral data informs coverage and pricing decisions.

Predictive Analytics for Loss Prevention

Predictive analytics represents a strategic evolution in the insurance industry’s relationship with risk, shifting the focus from compensating policyholders after losses occur to preventing those losses from materializing in the first place. By analyzing historical claims data, weather patterns, infrastructure conditions, economic indicators, and policyholder behavior, predictive models identify concentrations of risk that are likely to produce future losses and enable targeted intervention before damage occurs. A commercial property insurer can use predictive analytics to identify buildings whose fire suppression systems are likely to fail based on age, maintenance patterns, and equipment manufacturer recall data, then dispatch risk engineers to inspect and recommend improvements before a fire causes a catastrophic loss. This proactive approach reduces claims costs, improves policyholder safety, and differentiates the carrier as a value-added risk management partner rather than a passive claims payer.

Catastrophe modeling represents the most computationally intensive application of predictive analytics in insurance, combining atmospheric science, geological data, engineering models, and financial exposure information to estimate the potential impact of extreme events like hurricanes, earthquakes, floods, and wildfires. AI enhances traditional catastrophe models by incorporating real-time data feeds, improving spatial resolution, and enabling scenario analysis that accounts for the compounding effects of climate change on historical loss patterns. Insurers use these models not only to price catastrophe risk and manage reinsurance programs but also to guide underwriting decisions about which risks to accept, which to avoid, and which to accept only with specific loss prevention requirements. The ability to forecast losses before they happen and take preventive action transforms the insurer from a financial guarantor into an active participant in risk reduction, creating value for policyholders, shareholders, and the broader communities that benefit from reduced disaster impact. The distinction between automation and AI becomes particularly relevant here because predictive analytics requires genuine learning and adaptation, not simply the mechanical execution of predefined rules.

The Data Challenge in Insurance AI Adoption

Despite the compelling business case for AI adoption, insurers face significant data challenges that constrain the speed, scale, and effectiveness of their technology investments. Legacy systems that store policy, claims, and customer data in incompatible formats across multiple platforms create fragmentation that makes it difficult to assemble the unified, comprehensive datasets that machine learning models require to perform effectively. A large commercial insurer may operate separate systems for each line of business, each acquired company, and each geographic region, with different data schemas, naming conventions, and quality standards that prevent straightforward integration. Data cleansing, normalization, and migration projects consume enormous resources and years of effort before AI applications can begin delivering value, creating a frustrating gap between the promise of the technology and the reality of implementation.

Data quality compounds the integration challenge because AI models are only as reliable as the information they learn from, and insurance data is notoriously inconsistent, incomplete, and biased by historical underwriting and claims handling practices. Claims descriptions written by thousands of different adjusters over decades contain inconsistent terminology, varying levels of detail, and subjective assessments that introduce noise into training datasets. Historical underwriting data reflects the biases of past decision-makers, including geographic redlining, demographic discrimination, and inconsistent application of underwriting guidelines that varied by individual underwriter and office. Training AI models on this data without careful curation risks automating and amplifying historical inequities rather than correcting them, a problem that requires not just technical solutions but institutional commitment to data governance and ethical review.

Third-party data enrichment offers a partial solution to internal data limitations, but it introduces its own challenges around accuracy, privacy, and regulatory compliance. Insurers increasingly supplement their internal records with data from credit bureaus, telematics providers, IoT sensor networks, satellite imagery services, social media platforms, and public records databases to build more complete risk profiles. Each external data source must be evaluated for accuracy, timeliness, relevance, and compliance with data protection regulations that vary by jurisdiction and are evolving rapidly. The most successful insurance AI programs treat data strategy as a business capability rather than a technology project, investing in data governance frameworks, quality assurance processes, and cross-functional data stewardship teams that maintain the integrity of the information foundation on which all AI applications depend. Companies that view data as a strategic asset worthy of sustained investment outperform those that treat it as a byproduct of operational processes.

Algorithmic Bias and Fairness in Insurance Decisions

Algorithmic bias in insurance AI systems poses risks that extend beyond technical accuracy into fundamental questions of fairness, equity, and access to financial protection that regulators and consumer advocates are increasingly scrutinizing. Machine learning models trained on historical data inevitably absorb the biases embedded in that data, potentially perpetuating and scaling discriminatory patterns that human underwriters applied consciously or unconsciously over decades. A pricing model that incorporates zip code as a variable may effectively function as a proxy for race, producing systematically higher premiums for communities of color even when race itself is not an explicit input. The opacity of complex models makes these proxy effects difficult to detect and even harder to explain to regulators, policyholders, and the public, creating legal and reputational risks that can outweigh the accuracy improvements the models deliver.

Addressing algorithmic bias requires a multi-layered approach that spans model development, testing, deployment, and ongoing monitoring throughout the entire lifecycle of an AI system. Diverse development teams are more likely to anticipate and test for bias patterns that homogeneous teams might overlook, but diversity alone is insufficient without institutional processes that mandate bias testing before deployment. Techniques like fairness-aware machine learning, disparate impact analysis, and counterfactual testing help identify whether models produce systematically different outcomes for protected classes, and explainability tools help insurers understand which variables drive decisions and whether those variables function as prohibited proxies. The ongoing conversation about AI ethics and accountability applies with particular urgency in insurance because the industry’s decisions determine whether individuals and businesses can access the financial protection they need to participate fully in economic life. Regulators in multiple jurisdictions now require insurers to demonstrate that their AI models do not produce unfairly discriminatory outcomes, and the compliance burden will only increase as these frameworks mature.

Regulatory Landscape for AI in Insurance

Insurance regulation has always operated at the intersection of consumer protection and market competition, and the introduction of AI adds new dimensions of complexity that regulators around the world are working to address through evolving frameworks and guidance. In the United States, the National Association of Insurance Commissioners established the Big Data and Artificial Intelligence Working Group to study AI’s impact on the insurance sector and develop model regulations that states can adopt. The NAIC’s principles-based approach emphasizes transparency, fairness, accountability, and human oversight without prescribing specific technical requirements, reflecting the challenge of regulating a technology that evolves faster than legislative processes can accommodate. State insurance departments retain primary regulatory authority, creating a patchwork of requirements that carriers must navigate when deploying AI across multiple jurisdictions.

The European Union’s AI Act represents the most comprehensive regulatory framework affecting insurers operating in European markets, classifying AI applications by risk level and imposing graduated requirements for transparency, human oversight, data quality, and bias mitigation. Insurance underwriting and claims decisions may fall into the high-risk category, subjecting them to conformity assessments, registration requirements, and ongoing monitoring obligations that impose significant compliance costs. Insurers operating globally must reconcile the EU’s prescriptive approach with the principles-based frameworks favored by US and Asian regulators, designing AI governance programs flexible enough to satisfy multiple regulatory philosophies simultaneously. The regulatory trend across all jurisdictions points toward increased scrutiny of automated insurance decisions, particularly those affecting pricing, coverage eligibility, and claims outcomes for individual policyholders.

The evolving regulatory landscape creates both constraints and opportunities for insurers that develop robust AI governance capabilities early. Companies that build explainability, auditability, and fairness testing into their AI development processes from the outset will face lower compliance costs and fewer disruptive remediation projects when new regulations take effect. Those that treat governance as an afterthought risk costly model rebuilds, regulatory penalties, and reputational damage from publicized cases of algorithmic discrimination. Proactive regulatory engagement, where insurers participate in developing industry standards, share best practices with regulators, and voluntarily exceed minimum compliance requirements, builds institutional credibility that pays dividends during examinations, market conduct reviews, and public controversies. The carriers that view AI governance as a competitive advantage rather than a compliance burden will emerge from the current regulatory transition period with stronger market positions and deeper customer trust.

Privacy, Security, and Ethical Considerations

The ethical dimensions of AI in insurance extend beyond regulatory compliance into fundamental questions about what kind of industry insurers want to build and what relationship they want to have with the communities they serve. AI systems in insurance process deeply sensitive personal information: medical histories, financial records, driving behavior, home security footage, and biometric data from wearable devices. The concentration of this information in AI-powered analytics platforms creates privacy risks that require not just technical safeguards but organizational cultures that treat policyholder data as a trust rather than an asset to be exploited for maximum commercial advantage. Data minimization principles, where insurers collect and retain only the information necessary for specific, disclosed purposes, provide a foundation for responsible data practices, but the temptation to accumulate and monetize granular personal data grows as AI capabilities expand.

Cybersecurity threats targeting insurance AI systems represent a growing risk category that the industry must address with the same rigor it applies to other operational hazards. AI models themselves can be attacked through adversarial inputs designed to manipulate their outputs, data poisoning that corrupts training datasets, or model inversion attacks that extract sensitive training data from deployed models. A successful attack on an insurance fraud detection model could allow criminals to evade detection systematically, while a compromise of an underwriting model could produce systematically mispriced policies that destabilize the carrier’s financial position. The intersection of AI and cybersecurity creates both offensive and defensive implications: the same technologies that enhance insurance operations also expand the attack surface that adversaries can target, requiring security architectures that protect models, data, and decision pipelines as critical infrastructure.

The question of human agency in an increasingly automated insurance environment raises ethical concerns that technology alone cannot resolve and that deserve sustained attention from industry leadership. When an AI system denies a claim, declines to offer coverage, or sets a premium that a policyholder cannot afford, the affected individual deserves a meaningful explanation and a genuine avenue for appeal. Fully automated decisions that lack human review create accountability gaps where neither the algorithm nor any individual person bears responsibility for outcomes that may be wrong, unfair, or contextually inappropriate. Insurers must design their AI systems with human-in-the-loop safeguards for consequential decisions, ensuring that automation enhances rather than replaces the professional judgment that policyholders and regulators expect. The ethical imperative is not to slow AI adoption but to ensure that the efficiency gains it delivers do not come at the cost of the trust, fairness, and human accountability that form the foundation of the insurance relationship.

Transparency with policyholders about how AI influences the decisions that affect their coverage, pricing, and claims experiences is an ethical obligation that also serves the business interest of building long-term trust. Insurers should disclose when AI systems are involved in underwriting, claims, and pricing decisions, explain in accessible language what data sources feed those systems, and provide clear pathways for policyholders to request human review of automated decisions they believe are incorrect. Consumer research shows that acceptance of AI in insurance nearly doubled from 20% in 2025 to 39% in 2026, suggesting that transparency and positive experiences are gradually overcoming initial resistance. Carriers that lead on transparency rather than waiting for regulatory mandates will build stronger customer relationships and position themselves favorably for the inevitable expansion of disclosure requirements across all major insurance markets.

Embedded Insurance and Parametric Models

Artificial intelligence is enabling entirely new insurance product architectures that would be impractical or impossible without automated underwriting, real-time data processing, and dynamic pricing capabilities. Embedded insurance integrates coverage seamlessly into the purchase of products and services, offering relevant protection at the point of transaction without requiring the customer to seek out, compare, and purchase a separate insurance policy. When a consumer buys an airline ticket, rents equipment, purchases electronics, or books a vacation rental, AI-powered systems can instantly assess the risk, generate a tailored coverage offer, underwrite the policy, and bind coverage in seconds, all within the merchant’s checkout flow. The customer experience is frictionless, the conversion rates are high, and the distribution cost is a fraction of traditional agent or broker channels.

Parametric insurance represents another AI-enabled innovation that replaces traditional loss adjustment with automatic payouts triggered by predefined events measured by objective data sources. Instead of filing a claim, documenting losses, and waiting for an adjuster’s assessment, a parametric policyholder receives automatic payment when specified conditions are met: an earthquake exceeding a defined magnitude, rainfall below a threshold during a growing season, or wind speeds surpassing a contractual trigger in a geographic zone. AI and satellite data power these products by improving the accuracy of trigger calibration, reducing basis risk between the index measurement and actual losses, and enabling the design of increasingly granular parametric products for niche markets. The combination of embedded distribution, parametric triggers, and AI-powered underwriting is creating an insurance ecosystem where coverage can be purchased in seconds, priced to the individual, and settled without human intervention, a vision of insurance that would have been unimaginable a decade ago.

Building an AI-Ready Insurance Organization

Implementing AI effectively in insurance requires more than purchasing technology; it demands organizational transformation that spans strategy, culture, talent, data infrastructure, and governance frameworks. The most common failure pattern in insurance AI adoption is deploying sophisticated models on top of fragmented data systems and siloed organizational structures, producing pilot projects that demonstrate potential but never scale to enterprise production. Research indicates that while 88% of auto insurers and 70% of home insurers report using or planning to use AI, only 7% have successfully scaled AI systems into full production, revealing a massive gap between intent and execution that reflects organizational rather than technological barriers. Closing that gap requires executive commitment, cross-functional collaboration, and a willingness to redesign workflows around AI capabilities rather than simply inserting AI tools into existing processes.

Talent strategy is among the most critical and most neglected dimensions of insurance AI readiness, because the industry competes for data scientists, machine learning engineers, and AI product managers against technology companies, financial services firms, and startups that often offer more attractive compensation and career paths. Insurance carriers need professionals who combine technical AI expertise with domain knowledge of insurance operations, regulation, and customer needs, a combination that is rare and difficult to develop through training alone. The most effective organizations build hybrid teams that pair data scientists with experienced underwriters, claims professionals, and actuaries, creating collaborative environments where technical expertise and domain knowledge inform each other continuously. Investing in upskilling existing employees to work effectively with AI tools is equally important, because the value of AI systems depends on frontline professionals who understand their capabilities, limitations, and appropriate use cases.

Governance frameworks provide the guardrails that ensure AI systems operate within acceptable boundaries of accuracy, fairness, transparency, and regulatory compliance throughout their entire lifecycle. A comprehensive AI governance program defines clear ownership and accountability for every model, establishes performance monitoring and bias testing requirements, mandates human review thresholds for consequential decisions, and creates escalation pathways when models produce unexpected or concerning outputs. The carriers that invest in governance infrastructure before scaling their AI deployments avoid the costly remediation cycles that plague organizations that discover compliance gaps, bias issues, or performance failures only after models are operating in production at scale. Industry bodies, including the NAIC and European regulatory authorities, increasingly expect insurers to demonstrate mature governance capabilities as a condition of regulatory approval for AI-driven products and processes.

The Future of Artificial Intelligence in Insurance

The next wave of AI innovation in insurance will be defined by the emergence of agentic AI systems that can execute multi-step workflows autonomously, making decisions and taking actions that currently require human coordination across multiple departments and systems. Today’s AI tools largely operate within narrowly defined tasks: reading a document, scoring a risk, generating a response to a customer query. Agentic AI integrates these capabilities into systems that can manage an entire process from initiation through completion, such as receiving a claim notification, gathering relevant policy and loss information, analyzing damage, assessing coverage, detecting fraud indicators, calculating reserves, and communicating with the policyholder, all without human intervention for qualifying claims. Insurers allocate approximately 11.8% of their AI budgets to emerging agentic AI systems, a figure that will grow rapidly as the technology matures and demonstrates its ability to handle complex, multi-step insurance workflows reliably.

The integration of generative AI into insurance operations is moving from experimentation to production deployment, with applications that extend far beyond the chatbot use cases that dominated early adoption. Generative models draft policy wordings, create underwriting reports, compose claims correspondence, generate marketing content, and produce regulatory filings, handling the document-intensive work that consumes a disproportionate share of insurance professionals’ time. Nearly nine in ten insurers are now exploring generative AI tools, and over 55% have implemented them in claims, underwriting, and customer experience workflows according to industry surveys. The speed of adoption reflects the technology’s ability to produce high-quality insurance-specific text that requires minimal human editing, compressing processes that once required hours into minutes while maintaining the professional tone and technical precision that insurance communications demand.

Climate change and emerging risk categories are accelerating the demand for AI systems that can model unprecedented scenarios rather than simply extrapolating from historical patterns. Traditional actuarial methods calibrated to decades of loss experience become increasingly unreliable as climate patterns shift, creating exposure concentrations and loss severities that fall outside the range of historical observations. AI models that incorporate real-time atmospheric data, climate projection scenarios, and dynamic exposure mapping offer a path toward pricing and reserving approaches that account for a changing risk landscape rather than assuming stationarity. Cyber insurance faces a similar challenge, where the threat landscape evolves so rapidly that historical loss data becomes outdated within months, demanding AI systems that learn continuously from emerging attack vectors, vulnerability disclosures, and real-time threat intelligence feeds.

The insurance industry stands at an inflection point where AI transitions from a competitive advantage for early adopters to a baseline capability required for survival in an increasingly technology-driven market. Accenture’s research showing that 86% of insurance organizations plan to increase AI spending in 2026, with generative and agentic AI topping the investment list, confirms that the adoption curve has moved past the early majority and into mainstream commitment. The carriers that will thrive in this environment are those that combine technological capability with organizational agility, ethical governance, and a genuine commitment to using AI in ways that benefit policyholders as well as shareholders. The question is no longer whether AI will transform insurance but how quickly and equitably that transformation will unfold, and whether the industry will use the opportunity to build a more accessible, transparent, and responsive system of financial protection for individuals and businesses worldwide.

Key Insights

- According to Mordor Intelligence’s 2026 market analysis, the AI in insurance market is projected to grow from $26.3 billion in 2026 to $114.52 billion by 2031 at a 34.2% CAGR, reflecting accelerating demand across underwriting, claims, and fraud detection.

- Research compiled by AllAboutAI from 2025 industry surveys found that insurers using advanced AI report up to 75% faster processing speeds and 99% accuracy in risk assessments, demonstrating measurable operational transformation.

- An Insurance Business Magazine report from 2026 revealed that 86% of insurance organizations plan to increase AI spending in 2026, with consumer acceptance of AI in insurance nearly doubling from 20% in 2025 to 39% in 2026.

- According to Fortune Business Insights market research, North America dominated the AI in insurance market with approximately 40% of global market share in 2025, driven by strong adoption of advanced analytics and digital insurance technologies.

- Data from CoinLaw’s 2025 insurance industry analysis indicates that AI improves underwriting accuracy by 54%, with 47% of insurers now using predictive modeling for risk assessment and 58% deploying AI in cyber underwriting.

- The NAIC’s regulatory overview confirms that AI is now deployed across underwriting, pricing, customer service, claims handling, marketing, and fraud detection, with state regulators actively developing governance frameworks to ensure consumer protection.

- Industry analysis from SNS Insider research shows that the U.S. AI in insurance market alone is projected to grow from $3.15 billion in 2025 to $21.23 billion by 2033, indicating concentrated investment in the world’s largest insurance market.

The convergence of these data points reveals an industry undergoing a structural transformation at remarkable speed. Market projections consistently forecast 30% or higher annual growth rates, indicating that AI investment in insurance is accelerating rather than plateauing. The technology is moving beyond pilot programs into production deployments that deliver measurable improvements in speed, accuracy, and cost efficiency across every major insurance function. The critical challenge ahead is ensuring that the rapid pace of adoption is matched by equally robust investment in data governance, algorithmic fairness, regulatory compliance, and human oversight frameworks that maintain the trust essential to the insurance relationship.

How AI Transforms Insurance Operations: A Comparative View

| Dimension | Traditional Insurance | AI-Powered Insurance |

|---|---|---|

| Transparency | Decisions based on underwriter judgment; explanations provided verbally or through standardized letters | Model-driven decisions with audit trails; explainability tools can trace outputs to specific inputs |

| Participation | Policyholders interact primarily through agents and brokers during sales and claims | Self-service portals, chatbots, and mobile apps enable 24/7 policyholder engagement across all lifecycle stages |

| Trust | Built through long-term agent relationships and brand reputation | Enhanced by consistent, fast, accurate service; challenged by algorithmic opacity and data privacy concerns |

| Decision Making | Relies on actuarial tables, underwriter experience, and rules-based systems with limited variables | Integrates hundreds of variables through machine learning, producing granular, data-driven risk assessments |

| Misinformation | Fraud detected through manual investigation and rules-based flags with high false positive rates | AI detects fraud through pattern recognition, network analysis, and behavioral analytics with greater precision |

| Service Delivery | Claims settlement requires days to weeks with multiple human touchpoints and adjuster visits | Straight-through processing enables hours-to-minutes settlement for qualifying claims with minimal human intervention |

| Accountability | Individual underwriters and adjusters are accountable for their decisions; clear chain of responsibility | Accountability distributed across model developers, data scientists, and business owners; governance frameworks still maturing |

Real World Examples Of AI In Insurance

Lemonade’s AI-First Claims Settlement Model

Lemonade built its entire insurance business model around AI-powered operations, deploying machine learning and chatbot technology to handle policy issuance, claims intake, and settlement with minimal human involvement. The company’s AI Jim chatbot famously processed and paid a renter’s insurance claim in approximately three seconds, becoming a landmark demonstration of straight-through processing capability in the insurance industry. According to Lemonade’s public filings and technology documentation, the system handles approximately one-third of claims without any human intervention, reducing operational costs per policy significantly compared to traditional carriers. The limitation is that Lemonade’s model works best for standardized, low-complexity personal lines products, and the company has faced challenges extending AI-driven efficiency to more complex commercial and specialty lines where human judgment remains essential.

Tractable’s Computer Vision for Auto Claims

Tractable developed an AI-powered computer vision platform that analyzes photographs of vehicle damage to generate repair estimates, deployed by major insurers and collision repair networks across North America, Europe, and Asia. The system was trained on millions of images of vehicle damage and repair outcomes, enabling it to identify affected parts, assess damage severity, and estimate repair costs with accuracy that approaches experienced human adjusters. According to Tractable’s published case studies, carriers using the platform have reduced claims cycle times by 50% or more while improving estimate accuracy and consistency. The technology works exceptionally well for standard vehicle damage but still requires human review for complex structural damage, total loss assessments, and situations where damage severity falls at the boundary between repair and replacement.

Shift Technology’s AI Fraud Detection Platform

Shift Technology built an AI-powered fraud detection platform specifically designed for insurance, deploying machine learning models trained on billions of claims to identify suspicious patterns across property, casualty, health, and specialty lines. The platform analyzes every incoming claim automatically, scoring it for fraud indicators and flagging suspicious submissions for investigation by human special investigation units. According to Shift Technology’s industry reports, insurers deploying the platform have increased fraud detection rates by over 75% while reducing false positive rates compared to rules-based systems. The challenge is that sophisticated fraud schemes evolve continuously, requiring constant model retraining and the integration of new data sources to maintain detection effectiveness against increasingly adaptive adversaries.

Case Studies

Case Study: Progressive’s Snapshot Telematics Program

Progressive Insurance faced the challenge of differentiating itself in a commoditized personal auto market where traditional rating factors produced similar pricing across competitors, leaving limited room for competitive advantage. The company developed Snapshot, a telematics program that collects driving behavior data through a plug-in device or smartphone app, feeding the information into machine learning models that calculate individualized risk scores based on hard braking, time of day, and miles driven. According to Progressive’s investor presentations and public disclosures, the program has collected driving data from over 50 billion miles, enabling pricing accuracy improvements that attract lower-risk drivers who benefit from behavior-based discounts while maintaining underwriting profitability. Critics note that telematics pricing raises surveillance concerns and may disadvantage drivers who must commute long distances or work night shifts for economic reasons rather than choice, creating fairness questions that regulators are beginning to examine.

Ping An’s OneConnect AI Ecosystem

Ping An, China’s largest insurer, confronted the operational challenge of serving hundreds of millions of policyholders across life, health, property, and casualty lines while maintaining service quality and controlling costs across a vast geographic network. The company built OneConnect, a comprehensive AI platform that integrates facial recognition for customer authentication, NLP for automated document processing, machine learning for underwriting and claims assessment, and computer vision for property and vehicle damage evaluation. According to Ping An’s technology subsidiary disclosures, the platform processes over 1.5 million claims annually with AI assistance, reducing average claims processing time by 80% and detecting fraud patterns across the company’s massive data ecosystem. The limitation is that Ping An operates within China’s regulatory environment, which has different privacy standards than Western markets, raising questions about the transferability of its data-intensive approach to jurisdictions with stricter data protection requirements.

Zurich Insurance Group’s AI Claims Triage

Zurich Insurance Group needed to accelerate claims handling in its commercial insurance operations, where complex claims involving multiple coverages, jurisdictions, and parties created processing bottlenecks that delayed settlement and increased costs. The company deployed an AI-powered claims triage system that uses natural language processing to analyze first notice of loss submissions, automatically extract relevant information, identify applicable coverages, assess initial severity, and route claims to the appropriate handling team based on complexity and required expertise. According to Zurich’s digital transformation reports, the system reduced initial claims processing time by approximately 40% while improving routing accuracy, ensuring that complex claims reach specialized adjusters faster and routine claims enter streamlined handling pathways. The ongoing challenge involves maintaining model accuracy as claim types evolve, particularly in emerging areas like cyber, climate liability, and supply chain disruption where historical training data is limited.

Frequently Asked Questions About Artificial Intelligence in Insurance

Artificial intelligence in insurance refers to the deployment of computational systems, including machine learning, natural language processing, computer vision, and predictive analytics, to automate and improve core insurance functions. These technologies enable insurers to assess risk, process claims, detect fraud, price policies, and serve customers with greater speed, accuracy, and consistency than traditional manual methods.

AI improves underwriting by analyzing hundreds of variables simultaneously, identifying complex risk patterns that human underwriters and traditional statistical models cannot detect. Machine learning models evaluate data from credit reports, telematics, IoT sensors, satellite imagery, and public records to produce granular risk scores that enable more accurate pricing and faster policy issuance, reducing underwriting cycle times by up to 80%.

AI accelerates claims processing by automating intake, damage assessment, coverage verification, and settlement for qualifying claims. Natural language processing extracts information from claim submissions, computer vision analyzes damage photographs, and machine learning models estimate costs and detect fraud indicators, enabling straight-through processing that settles routine claims in hours rather than weeks.

AI detects fraud through multi-layered analysis that combines machine learning pattern recognition, behavioral analytics, natural language processing of claim narratives, computer vision analysis of damage photos, and social network analysis that identifies connections between parties involved in suspicious claims. These techniques work in parallel to catch sophisticated fraud schemes that rules-based systems miss.

The primary risks include algorithmic bias that produces discriminatory pricing or coverage decisions, data privacy vulnerabilities from processing sensitive personal information, regulatory compliance challenges in evolving legal environments, model drift that degrades performance over time, and accountability gaps when automated decisions lack adequate human oversight.

Telematics programs collect real-time driving behavior data through vehicle-installed devices or smartphone apps, measuring speed, braking, acceleration, cornering, and time of day. Machine learning models analyze this data to calculate individualized risk scores, rewarding safe drivers with lower premiums while creating financial incentives for behavior modification that reduces overall loss frequency.

Embedded insurance integrates coverage offers seamlessly into the purchase of products and services at the point of transaction. AI enables this model by performing instant underwriting, dynamic pricing, and automated policy issuance within merchant checkout flows, creating a frictionless experience that eliminates the need for consumers to separately shop for and purchase insurance.

Computer vision analyzes photographs and video of damaged vehicles, properties, and other insured assets to assess damage severity, identify affected components, and generate preliminary repair or replacement estimates. The technology enables remote claims assessment without requiring physical adjuster visits, reducing cycle times and improving consistency across large claim volumes.

Regulatory frameworks vary by jurisdiction but are converging on principles of transparency, fairness, accountability, and human oversight. In the United States, the NAIC develops model regulations that states can adopt, while the European Union’s AI Act classifies insurance applications by risk level and imposes graduated compliance requirements for high-risk deployments.

AI pricing models can improve fairness by basing premiums on individual behavior rather than broad demographic categories, but they can also perpetuate historical biases embedded in training data or use variables that serve as proxies for protected characteristics. Insurers must implement bias testing, disparate impact analysis, and ongoing monitoring to ensure AI pricing complies with anti-discrimination requirements.

Parametric insurance pays automatic benefits when predefined conditions measured by objective data sources are met, such as earthquake magnitude or rainfall levels, eliminating traditional claims adjustment processes. AI enhances parametric products by improving trigger calibration, reducing basis risk between index measurements and actual losses, and enabling the design of increasingly granular products for specialized markets.

Small insurers can adopt AI through cloud-based platforms, insurance technology partnerships, and vendor solutions that provide AI capabilities without requiring large internal technology teams. Starting with focused applications like chatbot customer service, automated document processing, or fraud scoring allows smaller carriers to realize incremental benefits while building institutional AI competency over time.

AI will automate many of the transactional and administrative tasks that agents and brokers currently perform, such as quoting, policy issuance, endorsement processing, and basic claims reporting. This shift will redirect agent and broker value toward advisory services, complex risk consulting, relationship management, and advocacy during major claims, roles where human expertise and trust remain essential.

Insurance professionals need data literacy to interpret and challenge AI outputs, technical fluency to collaborate with data science teams, and domain expertise to ensure AI applications align with insurance principles, regulatory requirements, and customer needs. Critical thinking, ethical judgment, and relationship management skills become more valuable as AI handles routine analytical and administrative work.